Colling Finance Insight: 'Life After KATA Changes'

- 14 Jul 2022 3:21 PM

As of 1 September 2022, KATA taxpayers will only be allowed to invoice goods and services to individuals.

Invoices issued to companies will immediately exclude the invoice issuer from this tax payment method.

More than 300,000 small business owners will have to look for a new tax form - or find a new job.

Only a full-time self-employed person can be a KATA self-employed person - not a retired person, a person with a job elsewhere, a student, a mum (dad) on GYED.

Opportunities until 31 August 2022

The KATA framework has been retroactively increased to HUF 1.5 million per month

Anyone who has been active in all eight months can benefit from the 12 million limits, even if the invoiced amounts are only received after 1 September.

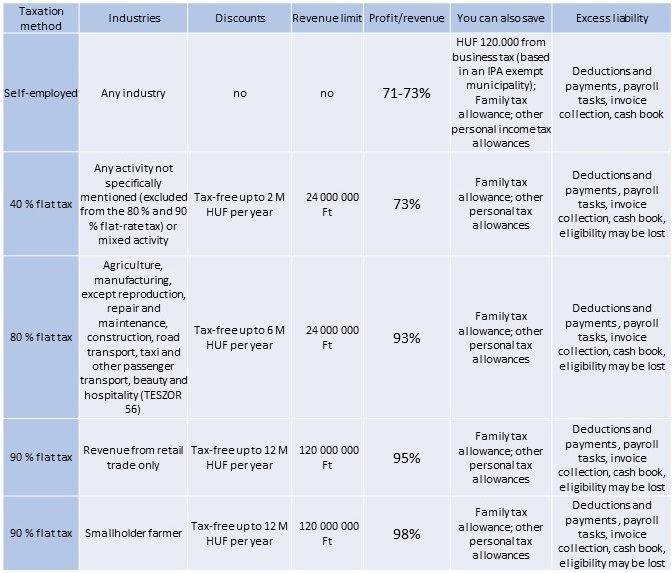

Tax options for sole proprietors after 1 September 2022:

Guaranteed minimum wage of 260 000 HUF, without personal income tax benefit, with an annual turnover of 12 million HUF, with a monthly accounting fee of 20.000 HUF - 40.000 HUF for the retail/web shop and KIVA Ltd.

For comparison purposes: the income / profit rate for a company under KIVA taxation is 69,5%, while the gross / net salary rate is 67%.

For whom is a normal self-employed status (with cost accounting) indicated?

* For those with high cost (raw material, subcontractor, operational) ratios.

* Those who can use a business establishment service in a municipality exempt from business tax (activity dependent).

* For those claiming high income tax deductions (e.g., mothers of four, under 25)

* Those who cannot meet the income thresholds

Who benefits from a flat tax?

* For low-cost providers, the 40 % cost ratio

* For workers in the beauty, goods and passenger transport and construction industries, the 80% cost ratio

80 % cost ratio for retailers, small online shops, distributors of own-produced products.

Flat tax tips:

* It is important to prepare a budget in advance to decide on the most appropriate form of taxation.

It is advisable to ask for the help of an accountant at the planning stage, as there are many details to keep in mind when making your choice.

* If you opt for a flat tax, in case you manage to get into the favorable 80-90% category, you should "clean up" your list of activities, and never invoice under a TOR number that (from the beginning of the year) reclassifies you into a worse category.

* Be careful with the income limits, because you may also be reclassified and, in addition, if you lose the possibility of a flat tax, you will not be able to opt for it again in the next two calendar years.

* You should pay attention to the HUF 12 million limit for the VAT exemption, because above this amount you will have to file a monthly VAT return.

* Anyone who is entitled to opt for flat-rate taxation both as a self-employed person and as a farmer may apply flat-rate taxation separately and simultaneously to the two types of activity

* A self-produced product is also considered a retail product.

* Invoices and other supporting documents relating to expenditure incurred to obtain the income must be kept until the right to tax retroactively becomes statute barred. On the one hand, it is compulsory, and on the other hand, it may be useful if the self-employed person is subject to retrospective taxation based on itemized cost accounting

* It is compulsory to keep a cash book or a ledger of receipts,

* The self-employed person must also produce and keep pay slips, just as if they were a company.

*A monthly payroll-related tax return must be submitted even if you have no income.

Click here to visit Colling online

1041 Budapest, István út 16.

office@colling.hu

LATEST NEWS IN specials